Dr Catriona Wallace speaking at Curious Thinkers 2022.

Artificial Intelligence is the fastest growing tech sector in the world, valued at US $327 bn in the last 12 months. It will also remove 85 million and generate 92 million jobs in the next two years. But who is leading the ethics of this powerful technology? The tech giants? Not likely. Government? Trying but about 5 years behind. And now commentators such as Stanford regard ‘Ethics Everywhere’ as the number one technology strategy priority for organisations.

So what is Responsible AI and how do you do it? Dr Catriona Wallace will share best practices in Responsible AI as well as sharing some super useful case studies. And most importantly Dr Wallace will discuss how you can step into being an Ethical Leader.

Leveraging the data-rich capabilities of the New Payments Platform (NPP), PayTo delivers insight rich, convenient and trusted payment arrangements for merchants, businesses and government agencies, while consumers benefit from having more control and visibility over payments set up from their bank account.

As PayTo commences rolling out to payments service providers and financial institutions over the coming months it is set to modernise the way bank accounts are used for payments, underpinning innovation for years to come in how we pay and get paid. Representing a step change in account-to-account payments, PayTo is much more than just a real-time alternative to direct debit. PayTo streamlines in-app payments, card-on-file arrangements, funding for digital wallet and buy-now-pay-later services and recurring e-commerce payments.

Accessing PayTo

Payments service providers, fintech and enterprise interested in initiating payments themselves, or on behalf of another third-party, can connect to PayTo via Cuscal. As a market leader in the NPP, Cuscal has the scale, experience, technical knowledge and trusted industry position to help payments service providers, fintech and enterprise compete and succeed with PayTo.

Merchants, businesses and government agencies interested in offering PayTo as a payment option for customers can now access PayTo services through a payments service provider connected to the Platform. Some of the leading innovators on the Platform today have integrated with PayTo through Cuscal’s Payment Initiator Service, building on top of our service to bring to life new innovative PayTo propositions.

Azupay

Established in 2019, Azupay is an Australian fintech focused on payment solutions using the New Payments Platform (NPP) technology, specialising in real-time payments using NPP and PayID to help government, business and consumers pay and get paid faster. www.azupay.com.au

Eway

Eway is a global omnichannel payment provider, processing ecommerce payments for merchants through a secure and reliable online payment gateway that makes it easy to accept payments from anyone, anywhere, from any device. www.eway.com.au

Ezidebit

Ezidebit is one of Australia’s leading online payment solution provider specialising in securely collecting Direct Debit, BPAY, EFTPOS and real-time payments for businesses. www.ezidebit.com

Ezypay

As one of Australia’s leading subscription payment providers, Ezypay offers a suite of easy-to-use subscription management services through their cloud-based payment platform, making it easy for businesses to settle payments and generate revenue through a standalone web interface, or directly integrated into a range of industry specific partner platforms. www.ezypay.com.au

GoCardless

GoCardless is a global leader in account-to-account payments, helping businesses accelerate the collection and management of recurring and one-off payments directly from customers’ bank accounts. With a global payments network and technology platform, GoCardless processes US$30 billion of payments for 65,000 businesses across more than 30 countries every year. www.gocardless.com

Monoova

Monoova supports scaling businesses with large, and often complex, ongoing transaction flows to fully automate how they receive, manage, pay and request payment of funds through one simple API integration. Its proprietary platform allows businesses to access a variety of payments functions, comprehensive reconciliation and reporting options and entirely customised real-time data. www.monoova.com

Paypa Plane

Australian fintech Paypa Plane helps banks and PSPs rapidly evolve product offerings without changing existing infrastructure through it’s simple ‘plug-in’ over the top bank-grade platform and white-label solutions, helping banks and PSPs create closer, more valuable and long term relationships with their small and medium business customers. www.paypaplane.com

Zai

Zai helps mid-market and enterprise-level business customers in the world of integrated financial services automate complex payment workflows and reconcile pay ins and payouts, helping them operate more effectively by saving time and money so they can scale and grow. www.hellozai.com

Cuscal was one of the founding financial institutions that established the New Payments Platform (NPP), Australia’s real-time payment system, and enabled over 60% of the financial institutions that were live on Day 1.

Since that time, Cuscal has strengthened its position as the market leader in NPP services, building a strong foundation of clients, industry relationships, expertise and scale over the last five years.

Cuscal currently:

Provides access to the NPP for over half of all financial institutions and payment service providers on the platform that offer real time payments to their customers

Processes 18% of payments made and 19% of payments received on the NPP

Cuscal is working closely with a large group of banks, payments service providers and software providers to support the ramp up of PayTo over the next few months. Cuscal’s PayTo development and implementation project has included many financial institutions and PSPs who wish to drive payment innovation and improved customer experiences using PayTo.

Cuscal is able to support a wide range of capabilities. We are about enabling competition. We provide services that let our clients innovate and develop their businesses. It has been a rewarding process to work with our financial institution and payment service provider clients to enable them to be the early adopters for PayTo.

The first group of financial institutions and payment service providers integrating with PayTo through Cuscal will go-live between July and September, followed by fast followers between October and December. The gradual ramp up of PayTo is expected to be completed in 2023 with full industry adoption.

Cuscal’s NPP infrastructure, scalable solution design and modular API services have made it possible for both existing and new clients who are focused on investing in innovation for their customers, to extend their NPP services to access PayTo, ensuring they are at the forefront of future payments innovation across subscription and bill payments, ecommerce and in app transactions, embedded finance and account funding, and the bulk disbursement of funds.

Cuscal has also partnered with software providers to ensure that Cuscal’s NPP Payments and PayTo services are integrated seamlessly into all clients’ digital channels to deliver an optimum customer experience.

Cuscal’s expertise and scale has also attracted clients who are nimble, innovative and focused to take advantage of one seamless onboarding to enable them to be first to market with Cuscal’s NPP Payments and PayTo services.

James Foster, Chief Executive Officer, Ezypay, commented:

We chose to partner with Cuscal as we knew they could deliver on our requirements to be live with PayTo on Day 1. We are a leading subscription payments fintech and it’s comforting to know that Cuscal’s vision for the future of payments in Australia is strongly aligned with ours.

NPP’s PayTo will be a new, digital way for merchants and businesses to initiate real-time payments from their customers’ bank accounts while allowing customers to see and control all recurring payments through their account. With the introduction of PayTo from mid-2022 all financial institutions that offer customer-initiated real-time payments will need to make significant changes to their back-office processes and technology in order to support receiving and actioning PayTo messages and payment initiation requests.

Ben Vivoda, Head of Client Services and Nathan Churchward, Head of Product Emerging Services, from Cuscal met virtually with members of the SAM Network to discuss this next phase of the NPP and the opportunities that PayTo will create.

When the New Payments Platform (NPP) rolled out on Tuesday, 13 February 2018 uptake was gradual as financial institutions rolled out NPP payment functionality to different customer segments and channels. However, as real-time payments have become more ubiquitous and innovative payment service providers have been enabled on the NPP, the growth trajectory of the platform has gone from strength-to-strength.

As one of a very small group of payment service providers to be enabled on the NPP, payment automation specialist Monoova recognised the potential of the platform early, partnering with Cuscal to access the platform and automate many of the manual processes that occur ‘before’, ‘after’ or ‘around’ payments which can be an obstacle to growth for scaling businesses.

From mid-2022 the next phase of growth for the platform commences with the launch of PayTo, enabling a broad range of use-cases which will provide a springboard for future payments innovation. Once again Monoova will be at the forefront of NPP-enabled innovation, with Monoova’s clients to be amongst the first in Australia to be able to initiate payments from a funding account with the payer customer’s authorisation.

This case study looks at how Monoova has innovated on top of Cuscal’s NPP and PayTo solutions to bring to life truly unique propositions that make managing business payments easy, providing clients with access to a true end-to-end payment automation solution that leverages all the capabilities of the NPP as well as Cuscal’s scale, expertise and trusted industry position to initiate, process and receive real-time payments.

The face of payments in Australia has changed dramatically over the last twenty to thirty years, with the pace of change set to accelerate as technological advancements revolutionise the way we make, receive and request payments.

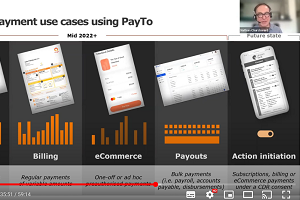

As the most frequently requested capability for the New Payments Platform (NPP), enabling the capabilities required to support third-party payment initiation from bank accounts has been a key priority for the payments and banking industry. Known as PayTo, this service will leverage the infrastructure of the NPP to drive the next phase of growth for the Platform.

PayTo will lead the use of embedded, pre-authorised payments from bank accounts in Australia, supporting a diverse range of payment use cases. It will provide consumers and businesses greater confidence, certainty and control over account-to-account payments as they are moved seamlessly into the background.

While PayTo will be available from mid-2022, when shifts in payment technology occur you want to be at the front of the queue to gain a first mover advantage over competitors. To help payment service providers and enterprises plan for the introduction of PayTo this white paper looks at:

The origins of real-time payments in Australia and the future directions for the NPP;

The rapid uptake of payment initiation in the UK under Open Banking;

The value PayTo will deliver to consumers and businesses and what the user journey looks like from the end-user perspective;

The role different participants play in the PayTo ecosystem; and

What Cuscal is doing to enable the PayTo services that are required by payer banks and payment initiators.

Format: White paper

Audience: Payment service providers and enterprises that process a large volume of payments

Estimated reading time: 20 minutes

Under the government’s Digital Economy Strategy Australia is set to become “a leading digital economy and society by 2030”, with the Consumer Data Right (CDR) one of several initiatives designed to establish the right foundations to grow the digital economy.

Integrated data and technologies will make life easier for consumers and businesses, but enterprises face the challenges integrating legacy systems and infrastructure with real-time digital ecosystems. Cuscal can help enterprises bridge this gap, deploying new capabilities that support the collection, sharing, management and storage of consumer consent and CDR data. While our position at the centre of payments – as the leading provider of New Payment Platform (NPP) payment services to banks and payment service providers – means we are ideally positioned to help enterprises unlock new growth opportunities from the convergence of data and payment initiation services.

This white paper provides senior leaders and product owners with insights into some of the regulatory, technology, security and capabilities required to comply with the CDR today and how to unlock opportunities from the convergence of data and payments.

In this white paper you’ll learn more about:

What the CDR is, how it has evolved and what future legislative change may mean for Data Holders in designated industries, as well as for accredited Data Recipients;

How NPP capabilities are being enhanced and extended through the development of the PayTo service, supporting ‘write’ access for third party payment initiation from bank accounts in real-time, as envisaged under CDR;

What enterprises should consider to enable data-centric strategies that integrate with the CDR and real-time payments, and how Cuscal capabilities and payment expertise can facilitate participation across ecosystems;

Use cases demonstrating some of the ways in which the CDR and payment initiation can be applied to make life easier for consumers and businesses;

How Cuscal is assisting clients participate in the CDR with access to a suite of secure and robust capabilities for the collection, sharing, management and storage of data subject to CDR legislation; and

How Cuscal is enabling payment initiation services that are align with CDR and NPP PayTo frameworks for banks, payment service providers, fintechs and enterprises.

If you’d like to know more about how Cuscal can support your business participate in the CDR ecosystem and with real-time PayTo payment initiation, call 1300 650 501 or submit an enquiry.

Sydney, 18 March 2021 – Cuscal announced today that it will become the latest member of the Australasia chapter of the Financial Data and Technology Association (FDATA). Membership of FDATA will provide Cuscal with valuable advisory, regulatory and industry engagement opportunities through FDATA’s deep knowledge of Open Finance, network of global experts and position on working groups, advisory panels and task forces.

As a Consumer Data Right (CDR) intermediary, Cuscal is committed to supporting data holders, consumers and data recipients to connect safely and securely to unlock the value of data. Cuscal’s Collaborative Data Exchange will manage the technicalities of the CDR for data holders and data recipients, leaving enterprise to focus on one of the most powerful opportunities in Australian commerce. Forward intelligence from FDATA on key policy matters, changes and trends from Australia and across the globe will form part of the Collaborative Data Exchange’s program of continuous development, helping clients to respond to changes in the CDR, including the emergence of new regulation, expansion of the CDR to new designated industries, and updates to data-standards.

Commenting on Cuscal’s membership of the regional chapter, Richard Prior, CEO of FDATA, said:

FDATA is delighted to welcome Cuscal to our worldwide community of members. As Open Finance proliferates across the globe, FDATA shares Cuscal’s goal of enabling the future, supporting the delivery of Open Finance for Australia, and the enormous potential and ambition enshrined in the CDR.

Kieran McKenna, Chief Risk Officer at Cuscal, commented:

We’re delighted to be joining FDATA Australasia at this critical moment during the implementation of Open Banking in Australia. Through our membership we’re looking forward to representing the interest of our clients and engaging with FDATA’s community of members, the government, regulators, policy makers and other stakeholders to help guide the formulation of policies relating to Open Banking and Open Finance in Australia.

About FDATA

The Financial Data and Technology Association (FDATA) is a not-for-profit representing fintechs operating in Open Banking and Open Finance. FDATA work with government, policy makers, and regulators to implement a fair and ethical competitive landscape that promotes competition, innovation, and better consumer outcomes.

About Cuscal

For more than 50 years Cuscal has championed competition in banking and payments in Australia, leveraging our scale, banking knowledge, technical expertise and regulatory experience to deliver reliable and secure solutions that supports the flow of transactional data between customers and enterprises, ensuring fair access to the Australian payments and banking ecosystem.

Media contact

Simone Shields, sshields@cuscal.com.au

In July 2020, the New Payments Platform (NPP) celebrated the registration of the 5 millionth PayID. In reaching this milestone I thought it would be interesting to look at the correlation between PayID registration and customer use and engagement. An analysis of the data we’re seeing for payments processed by Cuscal’s NPP solution tells a really positive engagement story.

Cuscal provides NPP services for 40 financial institutions that operate more than 50 banking brands. Partnering with Identified Institutions and NPP Participants our clients range in size, serve a variety of customers and are geographically distributed across Australia, offering a good representative sample of the Australian banking customer base. In fact, Cuscal processes more than 20% of all NPP payments and Cuscal’s clients have registered more than 25% of the 5 million PayIDs.

Our personal banking clients have been very successful in promoting PayID registration and Osko® to their customers, and now these banks, credit unions and their customers are benefitting from the convenience of making and receiving payments in real time.

Here are some interesting shifts that have happened between January and July 2020 in the transactions that Cuscal has processed for our personal banking clients.

Receiving payments

While the overall number of PayIDs registered is increasing, what is even more valuable are the numbers that show customers are actively sharing their PayID with others when they wish to receive money to their account and are receiving Osko payments with increasing regularity.

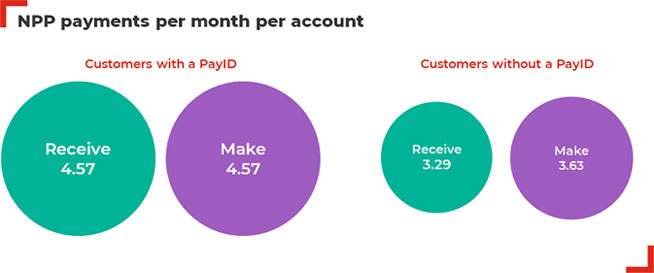

In July 2020, customers received an average of 4.6 payments to their PayID, up from 3.9 payments in January 2020.

14% of customers receive at least one payment each month to their PayID.

PayIDs that received at least one payment increased to 173,000 (25% up on January 2020).

9% of inward NPP payments are initiated using a PayID.

Looking beyond the payments that are received using a PayID, the numbers show that customers with a PayID also receive more NPP transactions generally, indicating that they are more engaged with their bank and the use of their account.

Customers without a PayID received an average of 3.3 NPP payments to their account a month.

When a customer has a PayID the average number of NPP payments received increases to 4.6 a month.

Since January, this represents an increase of 24% for customers with a PayID and only 9% for those without.

Making payments

Because PayID usage increases once people see how convenient it is, it’s interesting to note that customers that have a PayID also tend to make more payments overall.

Customers with a PayID make 4.6 payments per month from their account compared to customers without a PayID that make 3.6 payments.

Since January 2020, this is an increase of 24% for customers with a PayID and only 9% for those without.

Why this is important for banks

As technology continues to transform many aspects of our daily lives, and digital adoption accelerates in response to COVID-19, customers see the value in being able to manage their everyday banking needs at their fingertips. The ability to make or receive payments in real time from their accounts using the NPP with Osko and PayID are the types of services that customers now expect to find in digital banking. Banks that have actively promoted PayID and Osko services to their customers are their accounts and using their digital banking services. Ultimately this is leading to greater customer engagement and satisfaction.

Consent management will be a critical function for the successful rollout and uptake of the Consumer Data Right (CDR). In order to meet regulatory obligations, organisations will be required to demonstrate that they have have in place secure and robust consent management capabilities and infrastructure that ensures they can:

Safely and securely share consumer data;

Efficiently manage customer consent preferences;

Maintain customer privacy; and

Meet the evolving compliance requirements of the CDR.

This is essential to establishing and maintain consumer trust and for realising the objectives of the CDR.

Watch the video for more on the role of consent management in a digital economy.